Pagaya Technologies is leaning more on public securitization issuance because of volatility in private credit markets.

Market scrutiny around consumer credit performance and the potential for increased loan defaults in private transactions has contributed to a rise in spreads in the wider funding markets, Pagaya President and co-founder Sanjiv Das told Auto Finance News.

While neither Pagaya nor the financiers it works with are experiencing broad deterioration in credit, he said, spreads are widening as “investors want to protect themselves.”

“We pivoted a bit more toward public markets rather than private markets because of what’s going on with private credit,” Das said. In the “public markets, we have increased the size of our offerings and because of the huge demand that we are getting in terms of our flow, we are going more frequently to the market.”

“We pivoted a bit more toward public markets rather than private markets because of what’s going on with private credit.” — Sanjiv Das, Pagaya

Pagaya on May 13 issued a $385 million nonprime auto asset-backed securitization (ABS) deal, its third auto ABS deal in 2026. The fintech issued two ABS deals through the end of May 2025, according to CreditFlow, which monitors securities. The most recent deal also is larger than issuances in 2025.

“The public markets continue to be strong in terms of investors,” Das said. “Investor markets are wide open, so the cost of capital is marginally up, but not by a lot.”

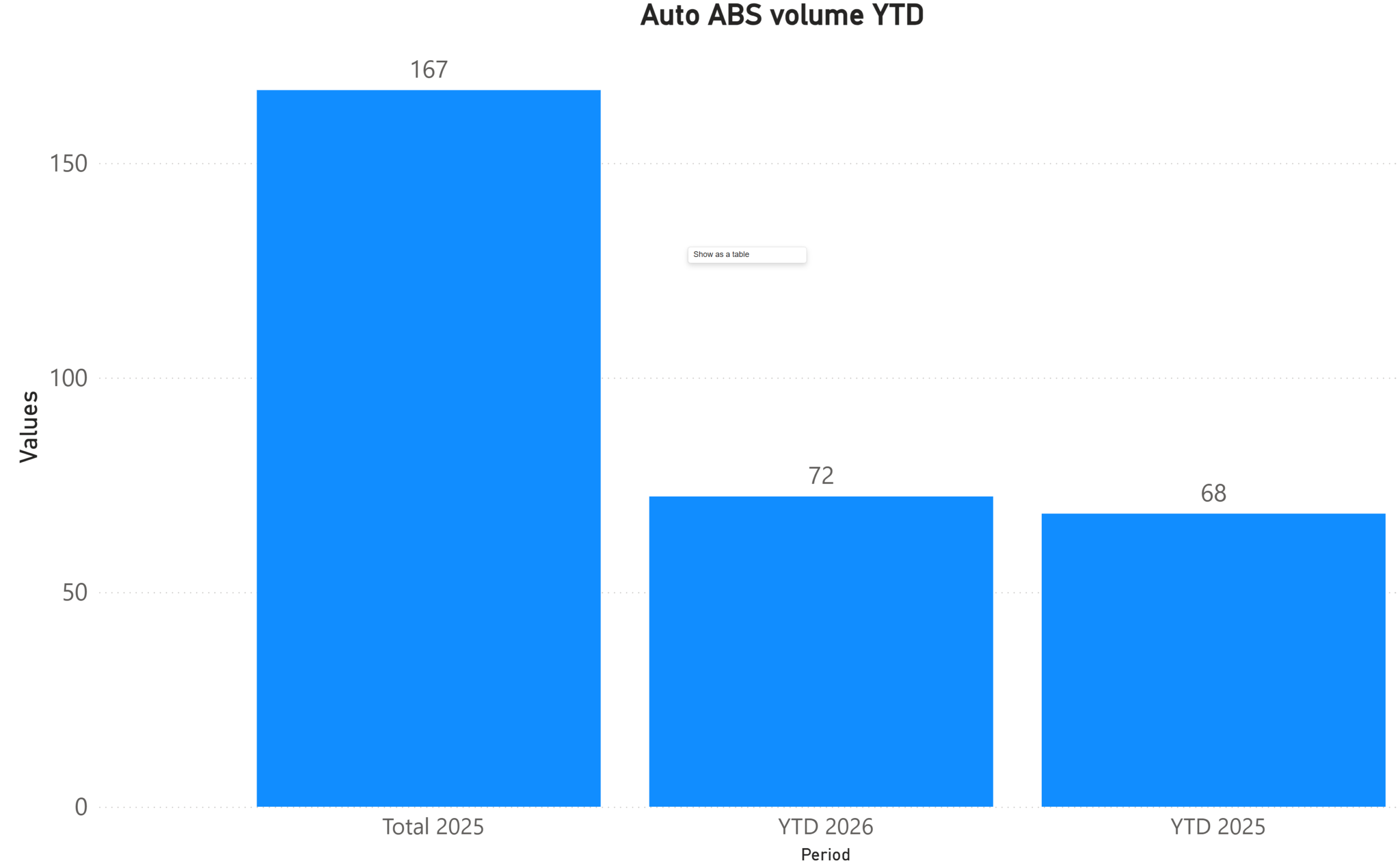

Total auto ABS issuance volume rose to $72.3 billion YTD through May 15, up 5.9% compared to the same period a year ago, while nonprime issuance rose by 9.2% year over year for that period, according to JPMorgan Securities data. Prime issuance ticked down 1.6% YoY.

Public ABS deals are the “most efficient source of capital” for many auto lenders, Robert Machanic, vice president of capital markets and treasury at Global Lending Services, said during a May 11 session at Auto Finance Capital Summit in Nashville, Tenn.

GLS’ “private credit opportunity through [forward-flow] sales is more of a liquidity strategy,” he said.

Pagaya recently signed on GLS, according to the fintech.

ABS for capital

Pagaya’s ABS transactions are fully pre-funded and are used to raise capital, Robert McDonald, managing director and head of credit solutions, said during another session at the summit. The fintech purchases loans that fall within its underwriting criteria from lenders and securitizes the loans to fund further originations.

“Because Pagaya Technologies is a platform, we operate a two-sided network where we have lending partners on one side, which we’re evaluating real-time application flow, which then turns into actual assets,” he said. “We need to ensure that we have capital available to acquire those assets.”

“We need to ensure that we have capital available to acquire those assets.” — Robert McDonald, Pagaya

An exception to the use of securitization for capital, McDonald said, is re-securitization of auto loans. Pagaya on March 24 closed a $450 million issuance that bundled auto loans that had been securitized in 2023 and 2024 into a fresh transaction for investors, according to a March 23 Kroll Bond Rating Agency new issue report.

“In that case, we use it as a funding tool,” he said, adding that diversified funding sources allow for flexibility in the market.

Pagaya plans to issue re-securitizations in auto every three to six months depending on market conditions, Das said, noting that it is another tool to optimize the balance sheet.

“You should be able to get better market performance if you call those loans and then re-securitize them, because now they are seasoned,” he said. “The two principal benefits [are] you get cash and you lower the cost of debt by re-securitizing seasoned loans.”

Auto run rate up 109% YoY

Pagaya is focused on optimizing pricing and coming to market in a “disciplined way,” Das said, noting that the ability to show counteroffers at the time of purchase are contributing to auto growth. Pagaya also increased its maximum loan term to 84 months to meet market demand, he said.

The fintech’s annualized run rate for auto reached $2.3 billion in the first quarter, up 109.1% YoY, according to its May 7 letter to shareholders. A longer tax refund season, in part, contributed to that growth, Das said. Tax refunds were larger on average this year but also faced delays.

“Auto has grown substantively in the last few quarters and we expect that growth to continue,” he said.

Find more coverage from Auto Finance Capital Summit here.