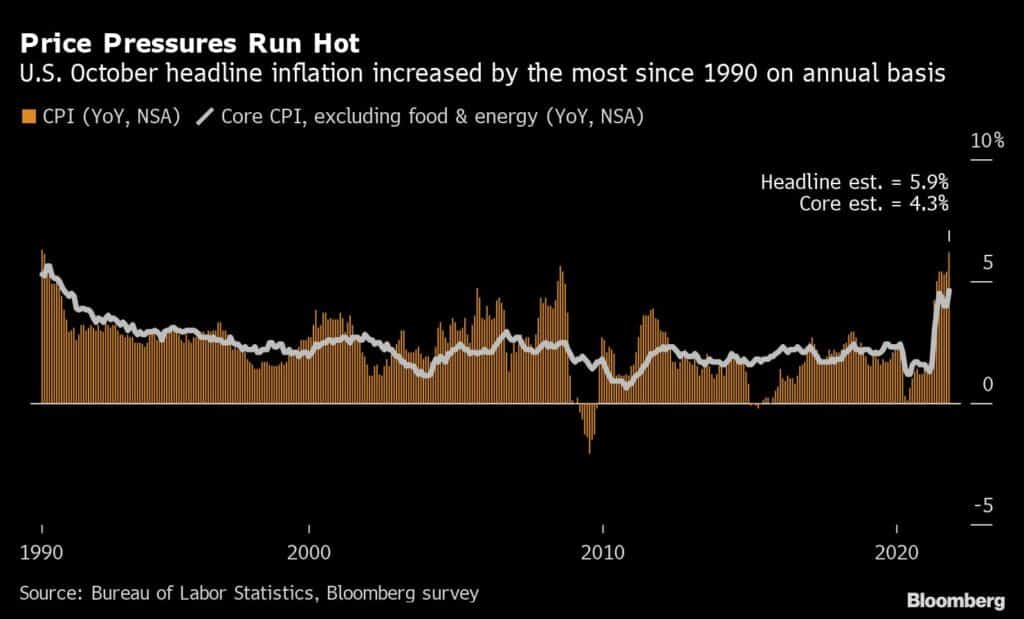

U.S. consumer prices rose last month at the fastest annual pace since 1990, cementing high inflation as a hallmark of the pandemic recovery and eroding spending power even as wages surge.

The consumer price index increased 6.2% from October 2020, according to Labor Department data released Wednesday. The CPI rose 0.9% from September, the largest advance in four months. Both advances exceeded all estimates in a Bloomberg survey of economists.

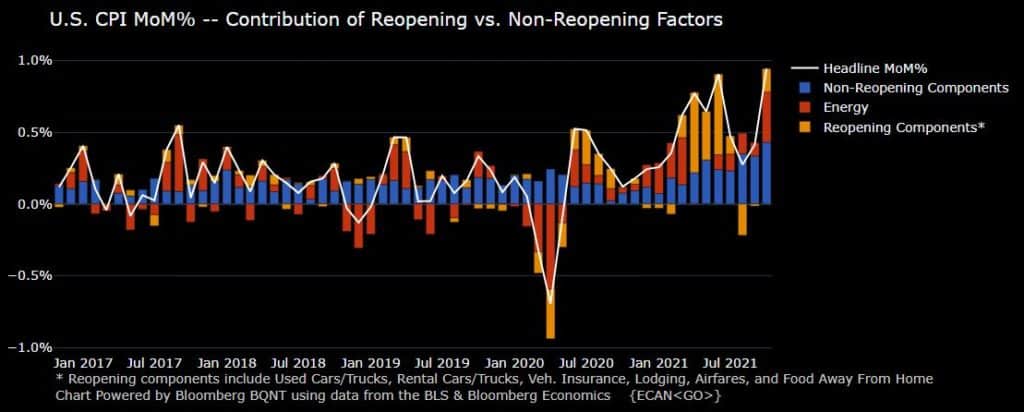

Higher prices for energy, shelter, food and vehicles fueled the supercharged reading and indicated inflation is broadening out beyond categories associated with reopening.

Stock futures dropped after the report, while the yield on the 10-year Treasury rose and the dollar strengthened.

Read more: U.S. 5-Year TIPS Breakeven Rate Rises to Record High

Against a backdrop of solid demand, businesses have been steadily raising prices for consumer goods and services at the same time supply chain bottlenecks and a shortage of qualified workers drive up costs.

Fed Pressure

The pickup suggests higher inflation will be longer-lasting than previously thought, putting pressure on Federal Reserve officials to end near-zero interest rates sooner than expected and potentially to quicken the pace of the bond-buying taper announced last week.

The data also threaten to exacerbate political challenges for President Joe Biden and Democrats as they seek to pass a nearly $2 trillion tax-and-spending package and defend razor-thin congressional majorities in next year’s midterm elections.

A report on Tuesday showed prices paid to U.S. producers also accelerated last month, largely due to higher goods costs, and adding to concerns about persistent price pressures across the globe.

In China, inflation at the factory level last month increased by the most in 26 years, while consumer prices in Brazil sped up by more than forecast.

Read more: China’s Inflation Risks Build as Producers Pass on Higher Costs

Excluding the volatile food and energy components, so-called core inflation rose 0.6% from the prior month and 4.2% from a year earlier. The annual increase was the largest since 1991.

Shelter costs — which are considered to be a more structural component of the CPI and make up about a third of the overall index — rose 0.5% in October, the most in four months as higher rents and home prices feed into the data. The cost of hotel stays increased.

Prices for new cars rose 1.4% last month as a global shortage of semiconductors continues to limit inventories and drive up costs. Used-vehicle prices jumped 2.5%.

Americans are also facing higher costs for basic necessities:

- Food up 5.3% from year ago, most since January 2009

- Gasoline rose 6.1% from September, biggest gain since March

- Electricity costs jumped 1.8%, largest monthly increase since 2014

- Fuel oil advanced 12.3% from prior month, most since 2007

Through the Company Lens

“We haven’t seen, I’ll say, any more resistance to our price increases than we’ve seen historically.” — McDonald’s Corp. CFO Kevin Ozan, Oct. 27 earnings call

“Looking at Q4, we expect our selling price actions to continue to gain traction, as we work to mitigate the raw material and logistics inflationary pressures we have experienced throughout the year.” — 3M Co. CFO Monish Patolawala, Oct. 26 earnings call

“We feel very comfortable that any inflation that is affecting our margin today, we have the ability to offset it.” — Chipotle Mexican Grill Inc. CFO John Hartung, Oct. 21 earnings call

“We have now announced pricing in nine out of ten categories, so very broad based.” — Procter & Gamble Co. CFO Andre Schulten, Oct. 19 earnings call

While most CPI categories rose, the cost of airfares declined for a fourth month and apparel prices were unchanged.

Wages have strengthened markedly in recent months — with some measures rising by the most on record — but higher consumer prices are eroding Americans’ buying power.

Inflation-adjusted average hourly earnings fell 1.2% in October from a year earlier, separate data showed Wednesday.

–With assistance from Chris Middleton, Reade Pickert, Sophie Caronello and Michael McDonough (Economist).

–By Olivia Rockeman (Bloomberg)