Credit unions, as a collective group, grew auto loan origination volume by about 7% in 2016, while all other loan providers — captives, banks, finance companies, and buy here pay here locations — saw volumes decline year over year, according to Michael Cochrum, vice president of analytics and advisory services at CU Direct.

Credit unions, as a collective group, grew auto loan origination volume by about 7% in 2016, while all other loan providers — captives, banks, finance companies, and buy here pay here locations — saw volumes decline year over year, according to Michael Cochrum, vice president of analytics and advisory services at CU Direct.

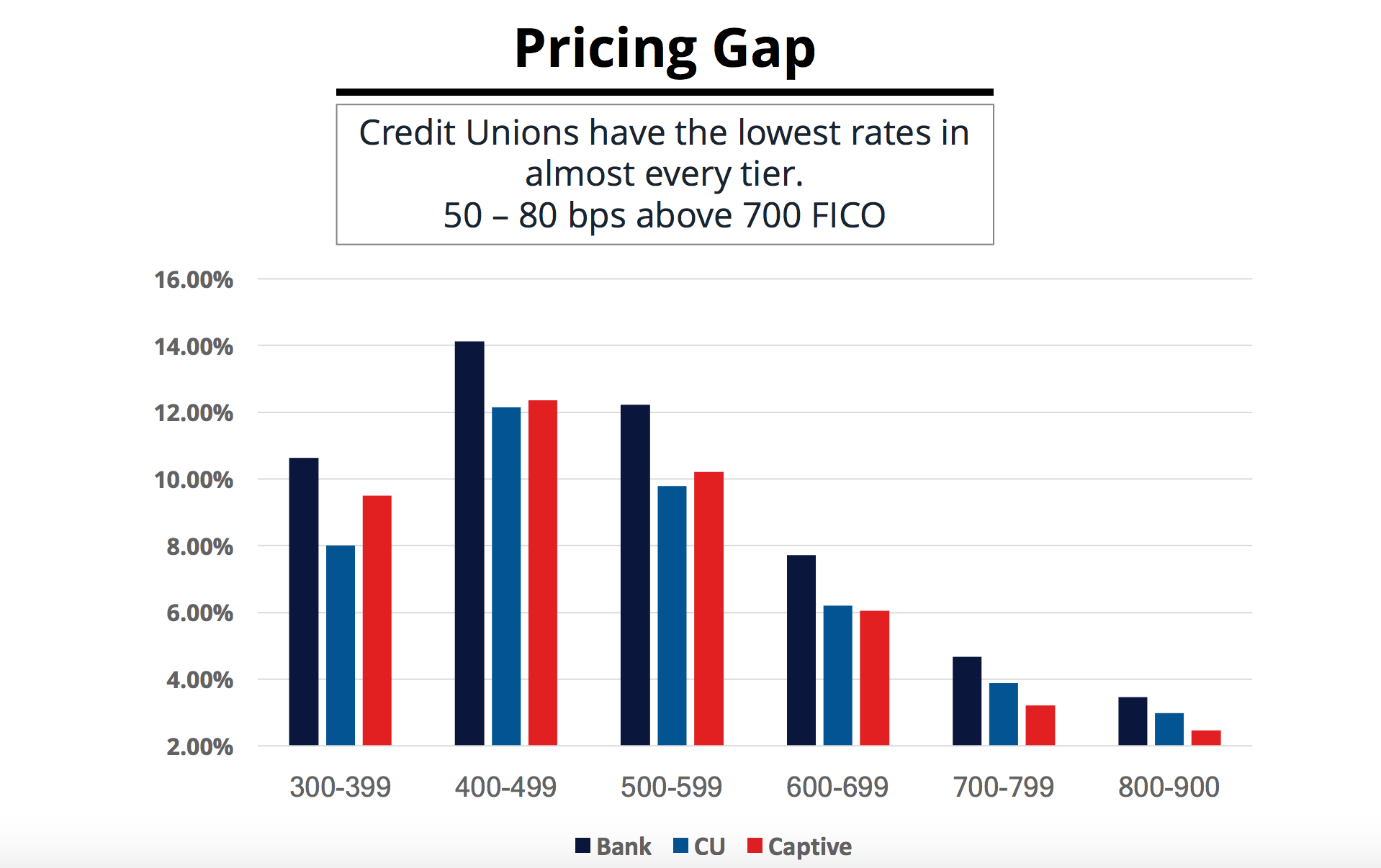

Those increased volumes largely remained in the prime end of the spectrum, at a 700 Fico score or above, Cochrum said during CU Direct’s state of the credit union auto lending market webinar last week. Credit union loan portfolios also had a higher percentage of prime loans — Fico scores of 600 and above — than banks and captives, which skewed slightly more subprime overall.

However, the data did not include leases and credit unions still make up a smaller percentage of overall loans, at 23% market share compared to 39% share from banks. Credit Unions will never compete with captives on leasing, Cochrum said, but his data showed that they can compete with banks on pricing.

“Captive finance companies are receiving manufacturer money to reduce the price of the loan,” he said. “There are certain loans captives are going to buy, and their are certain loans that dealers are going to send to their captives. All the rest of that business is going to go to a bank or credit union, so when you look at the spread and rates between banks and credit unions, we are competing over the same loans and we’re significantly under priced in the 600 to 699 range — it’s about 100+ basis points difference in price.”

That price differential means credit unions could increase rates by 25 or 30 basis points and still undercut their bank competitors, Cochrum said.

That price differential means credit unions could increase rates by 25 or 30 basis points and still undercut their bank competitors, Cochrum said.

Furthermore, because credit union portfolios skew prime on the risk spectrum, he recommended credit unions originate more volume in the subprime space and competitively increase rates to make up for the increased losses.

“We could increase our risk spectrum some by raising our price to cover the cost of the increased losses,” he said. “Those are some things that we need to consider, to form better relationships with our dealer partners.”