Fed pivot seen as bump, not dead end for reflation trade

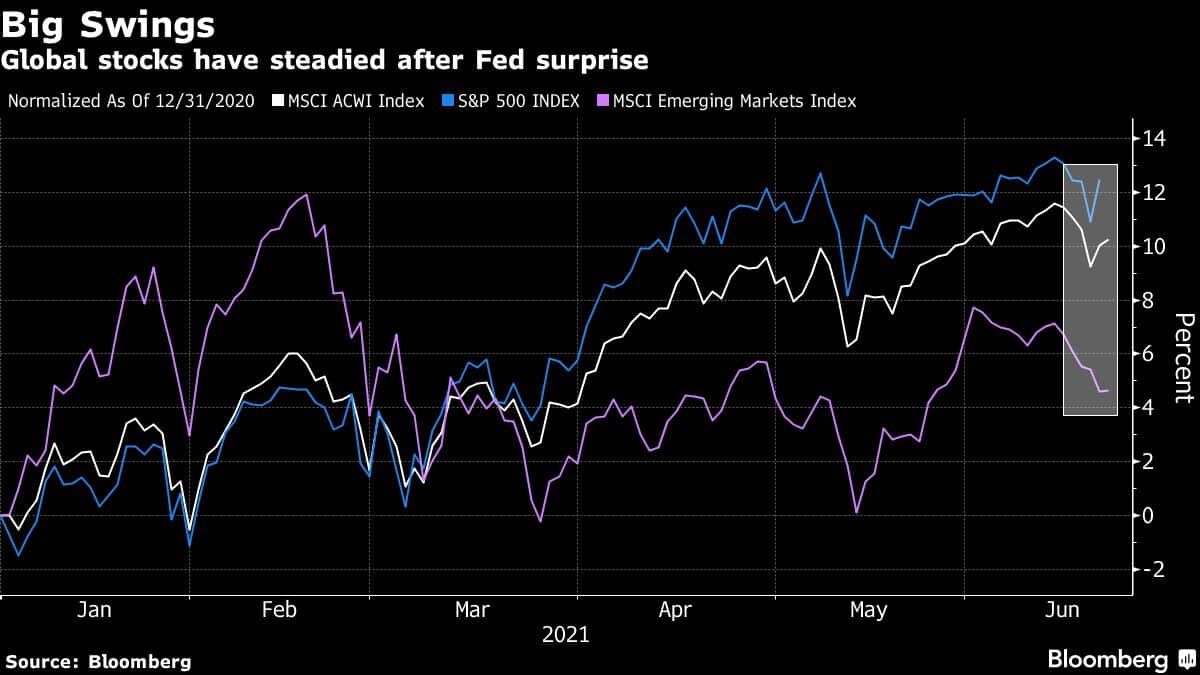

Markets were upended last week after the U.S. Federal Reserve signaled it would begin to dial back the stimulus that has fueled the recovery from the pandemic.

This slammed the brakes on the reflation trade — bets on stocks that benefit from faster economic growth — which had been humming along since November’s breakthrough vaccine announcements.

Now that traders have been able to take a few deep breaths and markets have regained their footing, strategists including Natixis Investment Managers and JPMorgan Chase & Co. say that it’s time to reload reflation trades. If anything, the latest wobbles actually strengthened their conviction.

The selloff was “bewildering” and a downright overreaction given the long runway until the first potential rate hike in 2023 and the unreliability of dot plots as a predictor, said Jack Janasiewicz, portfolio manager and strategist at Natixis, which has more than $1 trillion under management.

“This caused a nice quick flush out of some weak hands riding the reflation trade and likely reset positioning to a better place,” he said in an email. “As for the reflation trade, it remains intact. We still find many of the inflation-related worries as transitory which makes us give a more nuanced definition to our outlook: reflation, but not inflation.”

Natixis is sticking with cyclical positions and expects those trades to continue to work, with energy remaining a favorite, Janasiewicz added.

JPMorgan also sees buying opportunities after reflation trades suffered a “technically driven pullback,” strategists including Marko Kolanovic and Nikolaos Panigirtzoglou wrote in a note Monday.

“We expect the trade to resume and see this move as an opportunity to add exposure to cyclical equities and commodities,” they said. “Inflation is likely to continue to realize above both the Fed’s and markets’ expectations, driving bond yields higher and value outperformance.”

Emerging markets are also poised for further outperformance over developed peers, with JPMorgan raising its year-end target for the MSCI Emerging Markets Index to 1,550 from 1,450, implying about a 15% upside from current levels. The S&P 500, which fell for four straight sessions last week, has since rebounded to return to the same level as it was the day before the Fed announcement last Wednesday.

Still, the whipsawing market reactions to the Fed have spurred debate among investors over what to do if reflation trades falter.

Goldman Sachs Group Inc. strategists led by Christian Mueller-Glissmann see a greater focus on short-term rates sensitivity than in the past. Markets are looking to labor and inflation data for clues, as rapid improvements there might bring earlier Fed tightening, according to a note Monday.

“Coupled with slowing growth momentum, this might continue to weigh on risk appetite in the near term, although the repricing across reflationary assets has already been large,” they said.

The 2004 Model

The best yardstick for measuring out a path from here could be found by looking at the market’s performance in 2004, according to Morgan Stanley strategist Andrew Sheets. It offers the closest comparison to the current mix of a booming post-pandemic recovery, fiscal easing, high savings, low rates, higher inflation and tighter labor markets.

At that time, an extended malaise following the 2001 U.S. recession only troughed in 2003, followed by a surge in equity and credit markets as confidence returned. That means 2004 saw similar valuations in global equities, credit spreads and even volatility as those apparent today, Sheets noted in a report Sunday.

“In short, 2004 represents a more mid-cycle market after a strong, early-cycle rally,” he said. “It saw similar valuations, and what happened next is similar to some key Morgan Stanley forecasts: a pause in equities within an ongoing bull market, lower default rates but slightly wider spreads, modest dollar strength and more mixed equity leadership.”

While there are some key differences — 2004 was a U.S. election year, there was no quantitative easing and China and emerging-market dynamics were vastly different — one key lesson to take away is how quickly the Fed moved from preaching patience at the start of the year to hiking rates by June, pushing target rates up 425 basis points over the next two years.

“History always seems more orderly in hindsight,” he said. “Things can change.”

– By Eric Lam (Bloomberg)