Has Auto Loan Fraud Replaced Car Theft in America?

How Artificial Intelligence and Fraud Strategies Can Stem the Rising Tide of Fraud

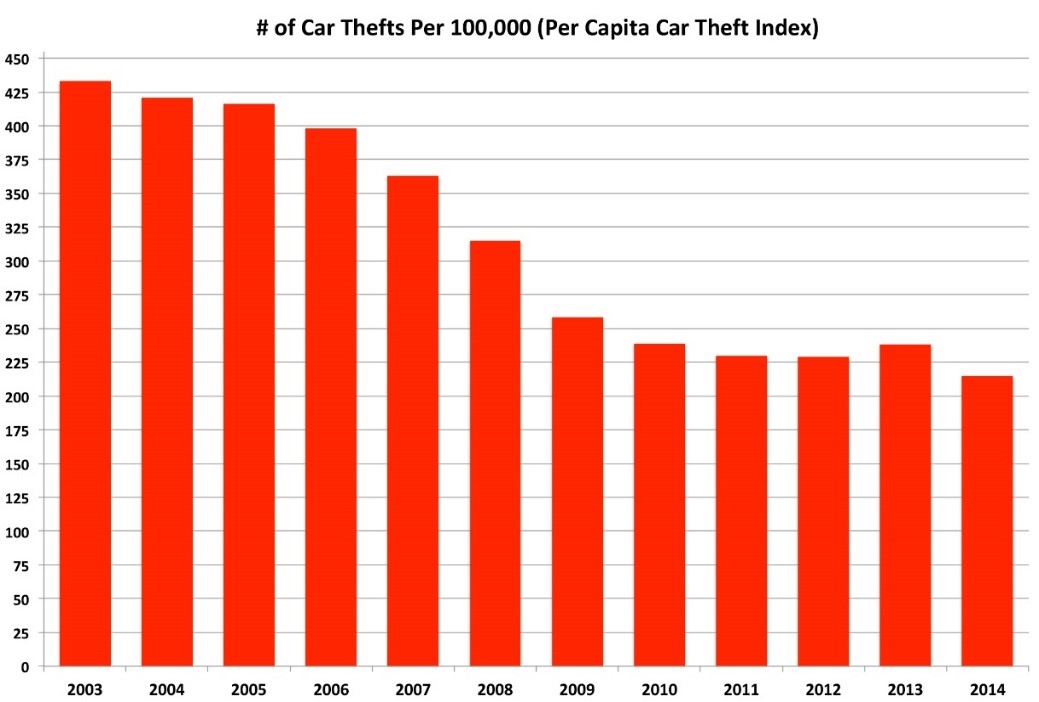

When it comes to auto theft, our cars are safer and more protected than ever. Investments by manufacturers to deter theft with engine immobilizers, LoJack, keyless entry, and other advancements have worked. In fact, the cars most commonly stolen today are older models that don’t have advanced technology – the favorite target in the U.S. is the 1997 Honda Accord.

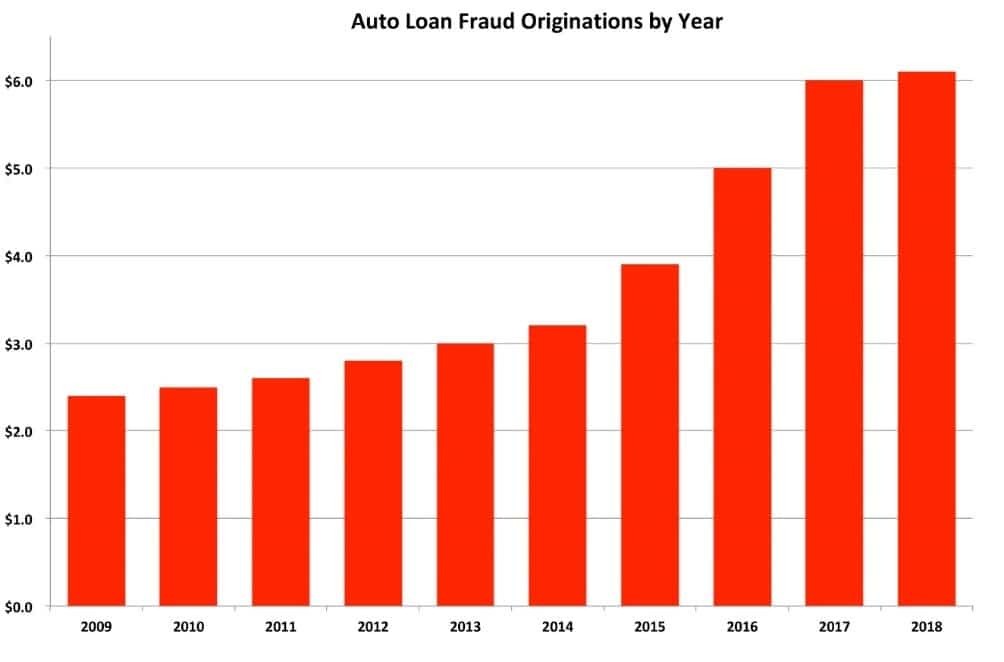

As auto thefts plummeted, theft by auto finance has increased. Crooks have found an easier way to commandeer cars than by breaking windows and jimmying locks. They discovered they can go to any car dealership and, armed with the right data, walk out with the keys to a brand-new car. It has become a $6 billion problem for auto lenders. But it hasn’t always been this bad. Auto lending fraud loss estimates have been climbing every year since 2009.

Fraud has increased because the investment in technology has been outpaced by the investment in anti-theft. Many lenders are starting to incorporate artificial intelligence to analyze millions of applications and the associated dealer activity to precisely identify which applications contain misrepresentations.

So, whether it is identity, income, employment or other misrepresentations about the information supplied – AI-enabled software alerts the lender to fraudulent activity more effectively than existing credit bureau or rule-based alerting solutions.

The Importance of a Fraud Manager

However, this enhanced technology should be used in tandem with documented policies and a proactive fraud manager. In many companies, fraud is considered a support function, with one or two fraud investigators fielding incoming calls from customers who are already victims of identity theft. This is a minimalist approach to fraud strategy that will let millions of dollars slip by. I worked with a bank recently that used this limited approach and discovered it had more than $100 million in fraud sitting on its books undetected and undiscovered until an auditor located the hidden fraud in a routine audit of charged-off losses.

Equipping fraud managers with application and dealer fraud scores should be considered a mission-critical component of your overall lending strategy. Following are reasons lenders should have a dedicated fraud management leader and supporting team:

- Reducing fraud losses: For the average auto finance lender, a fraud management team will prevent an average of $50,000 in fraud losses every day – that equates to more than $18 million a year. With sophisticated application and dealer scoring, plus responsibility for misrepresentation losses, that number increases substantially.

- Better balance between fraud prevention and customer experience: Finding the optimal balance between the impact on fraud and impact on the customer is like riding a seesaw. Executives will tell you one month to turn off fraud strategies to decline fewer customers for a better customer experience. But, by the next month, fraud losses will have increased, so executives tell you again turn up the fraud tools to drive down fraud. A fraud manager should guide your organization to achieve an optimal balance between the customer experience and fraud prevention.

- Advocate for preparing for the future. A fraud manager who is a strategic member of your organization will be willing to go head-to-head with marketing and sales to be the voice of fraud and go against the status quo, even when it’s an unpopular opinion. The manager will help keep the organization focused, have a pulse on the latest fraud trends, and guide you in investing in the latest fraud prevention technologies to avert future losses.

When auto lenders invest in technology and people to prevent theft at the same level as auto manufacturers, we will start to see a significant reduction in losses.

Frank McKenna is co-founder and Chief Fraud Strategist at PointPredictive, Inc. Frank is an advocate for fighting fraud and has worked with more than 100 banks, lenders and companies throughout the world, designing strategies, machine learning software and operational practices that help them reduce costs and increase efficiencies. He is an expert in the emerging fraud trends that consumers, lenders and auto dealers need to be aware of that contributed to the $6 billion fraud losses estimated to have impacted the auto lending industry.

Frank McKenna is co-founder and Chief Fraud Strategist at PointPredictive, Inc. Frank is an advocate for fighting fraud and has worked with more than 100 banks, lenders and companies throughout the world, designing strategies, machine learning software and operational practices that help them reduce costs and increase efficiencies. He is an expert in the emerging fraud trends that consumers, lenders and auto dealers need to be aware of that contributed to the $6 billion fraud losses estimated to have impacted the auto lending industry.